Payments features

Grow sales with a better payment solution

Fondy’s leading one-stop payment solution for marketplaces and platforms enables the means to move money without friction. We help you grow your business locally and internationally, allow you to seamlessly manage your money, easily split payments, and make payouts through a single API. With our multicurrency accounts, this process is simpler and faster.

Multicurrency accounts

Multiparty split payments

Instant settlements & payouts

Solutions for better business

Create a seamless customer experience and accept, settle, and track payments all in one place.

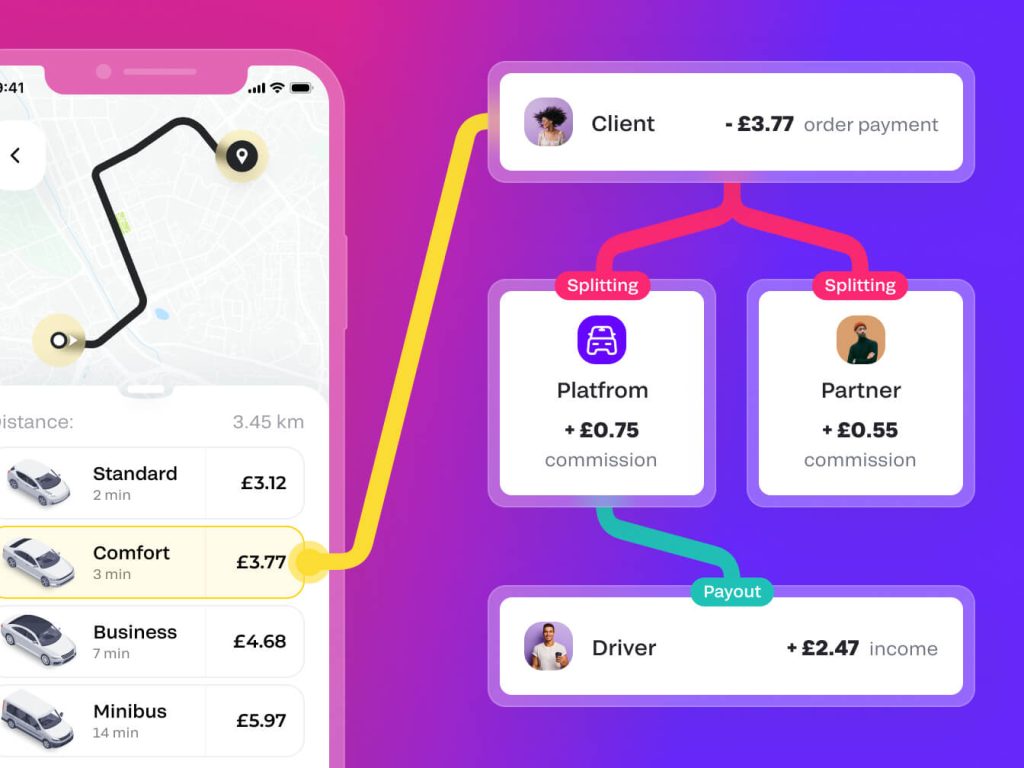

Flexible, reliable, easy multiparty split payments and payouts

With Fondy’s multiparty split payments and payouts you choose the recipients from platform users to global suppliers, and employees and we’ll take care of the rest.

Featured in

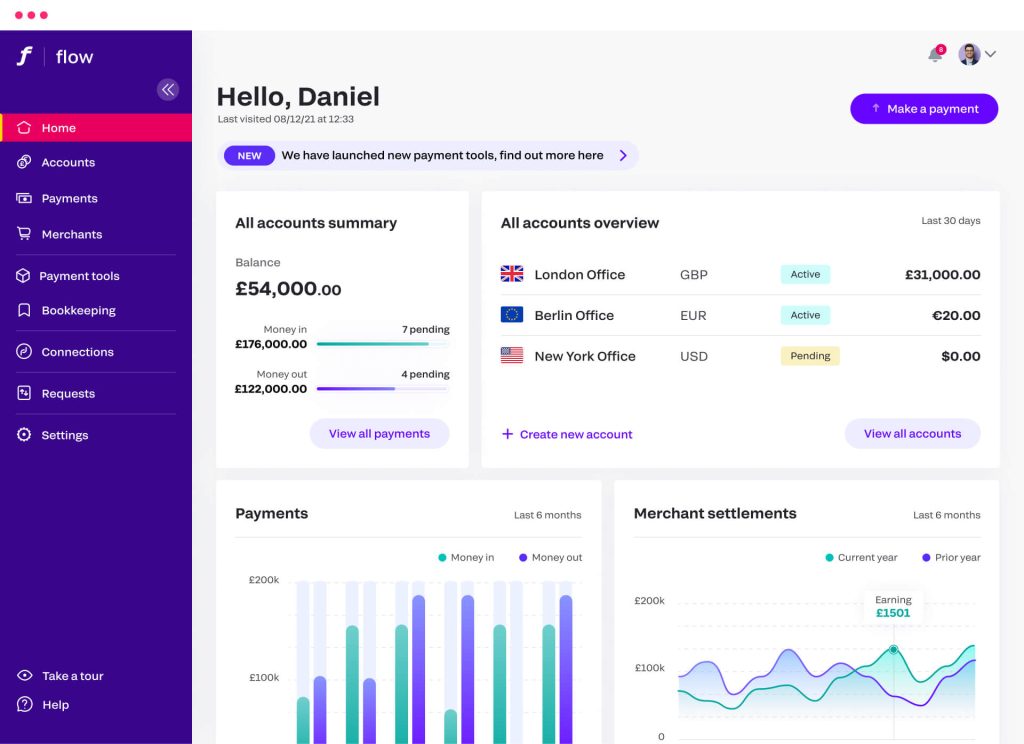

Managing payments

We make it easier for you to manage and control the flow of payments so you can do what you want, when you want. Through a single payment gateway API you can receive payments from your clients and pay out to your partners. Use seamless embedded finance infrastructure in one place.

Simpler billing & invoicing

Quickly send invoices via email, SMS or messenger, including WhatsApp and Facebook, as a link

Instant payouts

Choose the currency you want to payout in and split payouts to multiple parties, too

Collect more for less

Maximise revenues by setting up automated and recurring payments – this also reduces time on invoicing and chasing payments

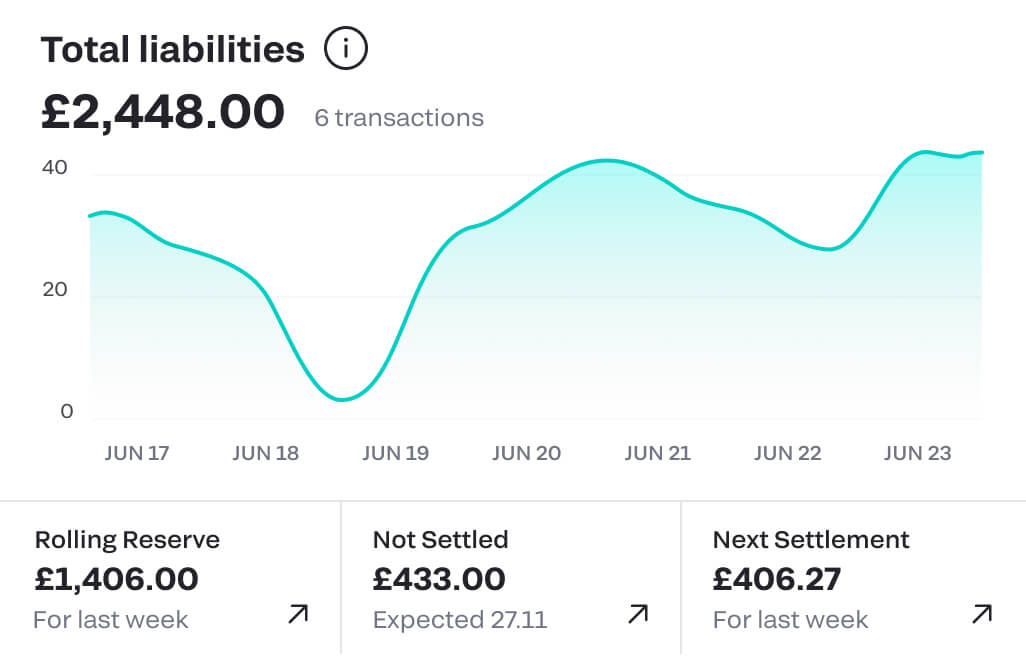

Figures at your fingertips

Have all the answers and information at your fingertips with up-to-the-moment view of all payments, plus income and profits

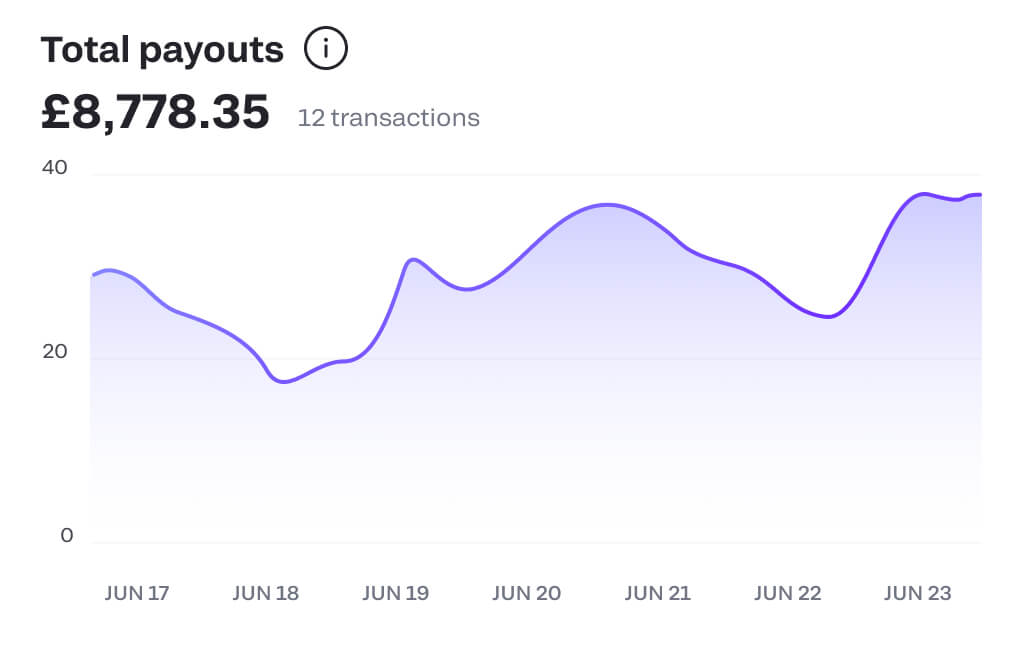

Instant settlements

No more waiting 5-10 days for payments to reach you – with Flow you will receive the money instantly into your Fondy account. You can even have multiple currency accounts. This gives you complete control to exchange it when you want or make payments in that currency. Plug-and-play banking products in one place.

Start accepting payments today

It’s so straightforward that you can sign up in the morning and accept payments from customers anywhere that same afternoon.

- Compatible with 15+ CMS platforms

- Simple API integration

- Supports 300+ payment methods

- Websites, apps and social media payments

- 23+ ready-made plugins

Customer stories

Fondy has been a great partner for us when it comes to expanding our acquiring capabilities in Eastern Europe, leveling up the region’s acquiring capabilities. Their experience in the market has been invaluable, helping us scale across the region.

We have started using Fondy for our eCommerce vaporisation and CBD stores, and we highly recommend this to other eCommerce businesses.

We are so pleased to have met such a reliable partner, we have enjoyed working alongside them for many years as the main payment system for card processing.

Finmap are long standing clients of Fondy and have found their features convenient and easy, particularly their API and subscription facility for recurring payments.

We chose Fondy’s payment service to solve an issue with receiving payments from different countries. Now we can instantly receive payments in any currency.

Everything in our store – from the brands to the products are of the utmost quality. We strive for perfection from start to checkout. Fondy support us to maintain our high standards.

So pleased to have found a reliable partner like Fondy. We are happy with their services and hope to continue using them for years to come.

Get started today

Fondy makes it easy for customers to pay and simple for you to sell with all the flexibility and control you need

Open an account

Create a no-obligation account now and see how it works. You could even start trading today.

Request a demo

Request a demo of our gateway portal and Flow – our multicurrency accounts service today.